Fed Turns Hawkish, Signals Fewer 2025 Cuts: What This Means for Banks

The Federal Reserve announced yet another interest rate cut of 25 basis points yesterday despite persistent inflation. This lowered the Fed funds rates to the 4.25-4.5% range, which is now at the same level as in December 2022.

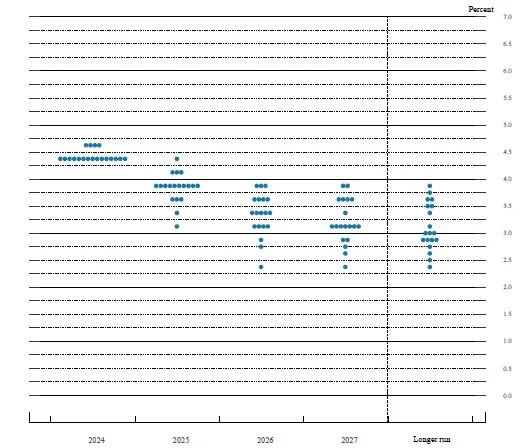

Further, the central bank scaled back the number of cuts it projects for 2025, signaling caution. The “dot plot,” which maps out policymakers' expectations for where interest rates could be headed in the future, showed only two interest rate cuts for 2025. This is lower than the four estimated during the September FOMC meeting and would bring rates close to 3.9% by 2025-end.

Fed’s Dot Plot

Fed chairman Jerome Powell said, “The slower pace of cuts for next year really reflects both the higher inflation readings we had this year and the expectation inflation will be higher.” Following this, the stock market plunged, with all major indexes ending the day in red. The rate-sensitive sectors, including the Financial Services, were among the worst performers in the S&P 500 Index.

Banks, the major constituents of the Financial Services sector, witnessed notable declines yesterday. The KBW Nasdaq Regional Banking Index and the S&P Banks Select Industry Index declined more than 5%. Shares of Wall Street biggies, including

JPMorgan

JPM,

Bank of America

BAC and

Citigroup

C, tanked more than 4%. Even regional bank stocks like

Comerica

CMA and

KeyCorp

KEY were down almost 5% yesterday.

What Else Did the Fed Signal?

In addition to next year’s reduction in interest rates, the Fed officials, through the dot plot, signaled two cuts in 2026 and 2027 each. This will bring the interest rates close to 3.4% by the end of 2026 (higher than the 2.9% previously forecasted during the September FOMC meeting) and 3.1% by 2027-end.

Additionally, the central bank came out with the latest Summary of Economic Projects (SEP). Per the latest SEP data, the U.S. economy is anticipated to grow at the rate of 2.5% this year and 2.1% in 2025.

Moreover, the Fed officials noted that “labor market conditions have generally eased, and the unemployment rate has moved up but remains low.” They lowered their expected unemployment rate to 4.2% for 2024 from 4.4% forecasted during the last update in September. Further, in 2025, the unemployment rate is estimated to be 4.3%.

The central bank increased the inflation target to 2.4% for 2024 from 2.3% predicted in September.

For 2025, the inflation will likely be 2.5%, a significant upward tick from the prior forecast of 2.1%. This indicates inflation is going to be stickier than previously expected. The Fed officials seem to have accounted for the incoming President’s potential policy-related decisions, including the stance on tariffs while predicting inflation for 2025.

How Will Banks Be Affected by the Fed Decision?

With potentially fewer interest rate cuts next year, banks will likely face extended periods of elevated funding costs. As the Fed started raising interest rates in March 2022, banks including JPM, BAC, C, CMA and KEY recorded a significant surge in net interest income (NII) and net interest margin (NIM). However, higher rates led to a jump in funding and deposit costs, eventually hurting banks’ NII and NIM growth beginning this year.

With the central bank lowering interest rates effective September 2024 and signaling four cuts in 2025, banks presented an optimistic view for NII and NIM for the upcoming quarters as funding costs started stabilizing. But now, because of fewer rate cuts, a solid NII and NIM expansion is less likely to occur next year.

Also, the lending scenario is not expected to improve much in 2025 compared with 2024, as rates will remain high for longer. Thus, demand for loans is expected to be modest. Further, asset quality is likely to continue to be a major headwind in 2025 as borrowers may find it difficult to repay loans.

Therefore, the operating environment for banks is not expected to be as rosy as it was projected earlier. A turnaround in banks’ financial performance will take time and is not expected before mid-2025.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC) : Free Stock Analysis Report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Citigroup Inc. (C) : Free Stock Analysis Report

Comerica Incorporated (CMA) : Free Stock Analysis Report

KeyCorp (KEY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research